Moncton Housing Market Forecast 2026 | Will Home Prices Rise or Fall?

A Deflationary Shift Most Realtors Aren’t Talking About

If you’re searching for a Moncton housing market forecast, you’re probably asking one simple question: Are home prices in Moncton going up, stabilizing, or starting to fall?

Here’s my honest take. I believe we are entering a more deflationary economic environment, and that has real implications for the Moncton real estate market, and Canadian housing more broadly. This may not be the popular narrative. Many will disagree. But I tend to approach markets through a data-driven lens, not headlines or sentiment. When I step back and look at the numbers objectively, the analytical side of me sees a pattern forming and I suspect we are entering a new deflationary phase. Let me walk you through what I’m seeing, and why the data points toward a structural shift rather than just short-term noise.

Inflation May Be Breaking Faster Than Expected

Most people follow government CPI reports. They come out monthly. They get debated on television. They influence headlines. But CPI is backward-looking and survey-based. Alternative real-time metrics like TruFlation tracks millions of live price data points across food, fuel, goods, and services. Instead of waiting for surveys, they measure what people are actually paying in real time. And what that data suggests is clear: Inflation pressure is cooling rapidly.

When inflation falls faster than expected, it often signals something deeper: demand is weakening. And housing is not immune to that. Let’s look at some recent data coming from our neighbours to the south.

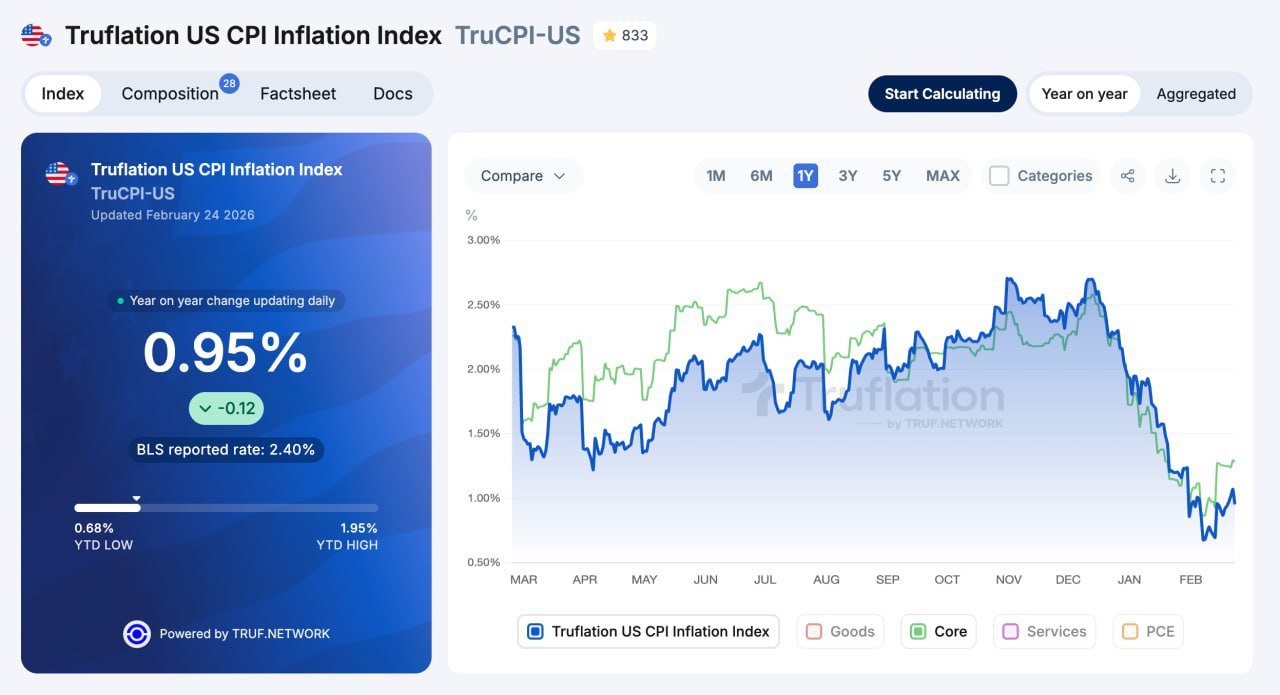

In the United States, inflation is traditionally reported through the Bureau of Labor Statistics (BLS) using the Consumer Price Index (CPI). The Federal Reserve aims to maintain price stability by targeting roughly 2% annual inflation. The theory is that modest inflation encourages economic activity, supports wage growth, and prevents stagnation.

According to the most recent BLS release, year-over-year inflation is reported at 2.40%. However, there is now an alternative real-time inflation measure called TruFlation that tracks millions of live price data points across categories like food, energy, goods, and services. Instead of relying primarily on survey sampling and lagged reporting methods, TruFlation aggregates high-frequency digital pricing data updated daily from over 80 million data points. This is the most accurate way to track inflation in 2026, not the report big Government wants you to believe. (2.40%)

As of February, TruFlation is showing inflation at just 0.95% year-over-year. That is a significant gap. This divergence suggests that price pressures may be cooling much faster than official reports indicate. If inflation is truly trending closer to 1% than 2.4%, it raises an important question: Are we entering a disinflationary phase or potentially something more deflationary?

Now layer in the rapid acceleration of artificial intelligence, robotics, automation, and productivity tools. These technologies are inherently deflationary. They increase output while reducing labor and production costs. When the cost of production falls across multiple sectors like energy, manufacturing, logistics, transportation, then asset pricing eventually adjusts and reduce accordingly in a free market. Real estate does not operate in isolation from broader economic forces. If productivity continues accelerating while consumer demand simultaneously softens, pricing pressure across asset classes, including housing, can follow. The next six to twelve months will be extremely telling.

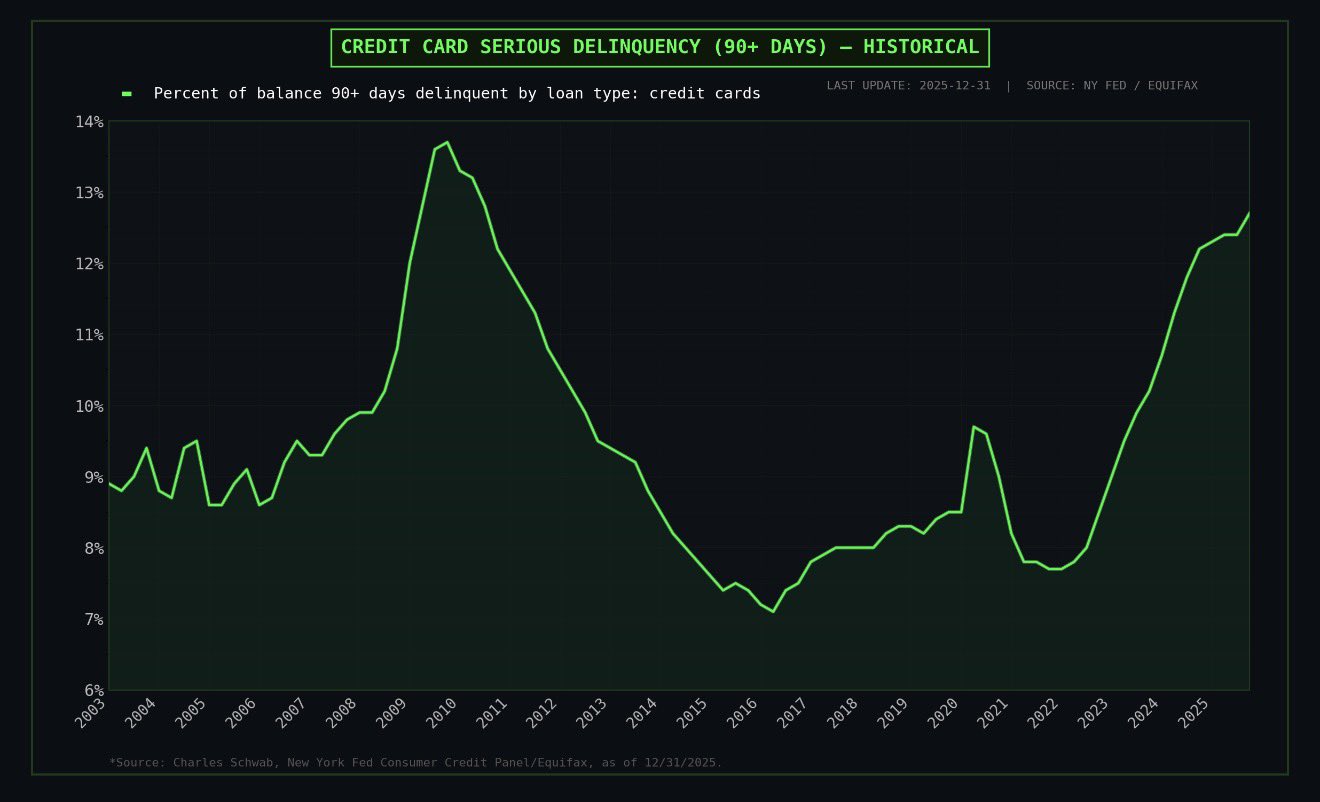

Consumer Stress Is Rising Beneath the Surface

Across North America, 90+ day credit card delinquencies are climbing back toward levels last seen during the 2008 - Global Financial Crisis. What makes this notable is that we are not currently in a declared recession. There are no collapsing banks or double-digit unemployment figures dominating headlines. On the surface, the economy appears relatively stable. But beneath the surface, financial strain is building and households are feeling it.

Total credit card debt has reached record highs. Interest rates on those balances often exceed 20%. At the same time, property taxes keep rising, insurance premiums are on the rise, heating and utility costs remain elevated, and ongoing maintenance expenses are not getting cheaper.

While wages have improved in some sectors, they have not fully kept pace with the cumulative rise in overall living costs. When household budgets tighten, many people bridge the gap with high-interest revolving debt. The challenge is that this type of debt compounds quickly and becomes increasingly difficult to service as balances grow. When consumers feel financially stretched, large discretionary decisions such as buying, upgrading, or investing in real estate are often postponed.

Why does this matter for a Moncton housing market forecast?

Because Canada is experiencing many of the same pressures, and in some cases Canadian household debt ratios are even higher. Historically, when consumer stress builds at a national level, housing demand tends to soften with a lag. Housing markets do not require a dramatic crisis to cool. They simply require buyers to become more cautious which is what this market feels like.

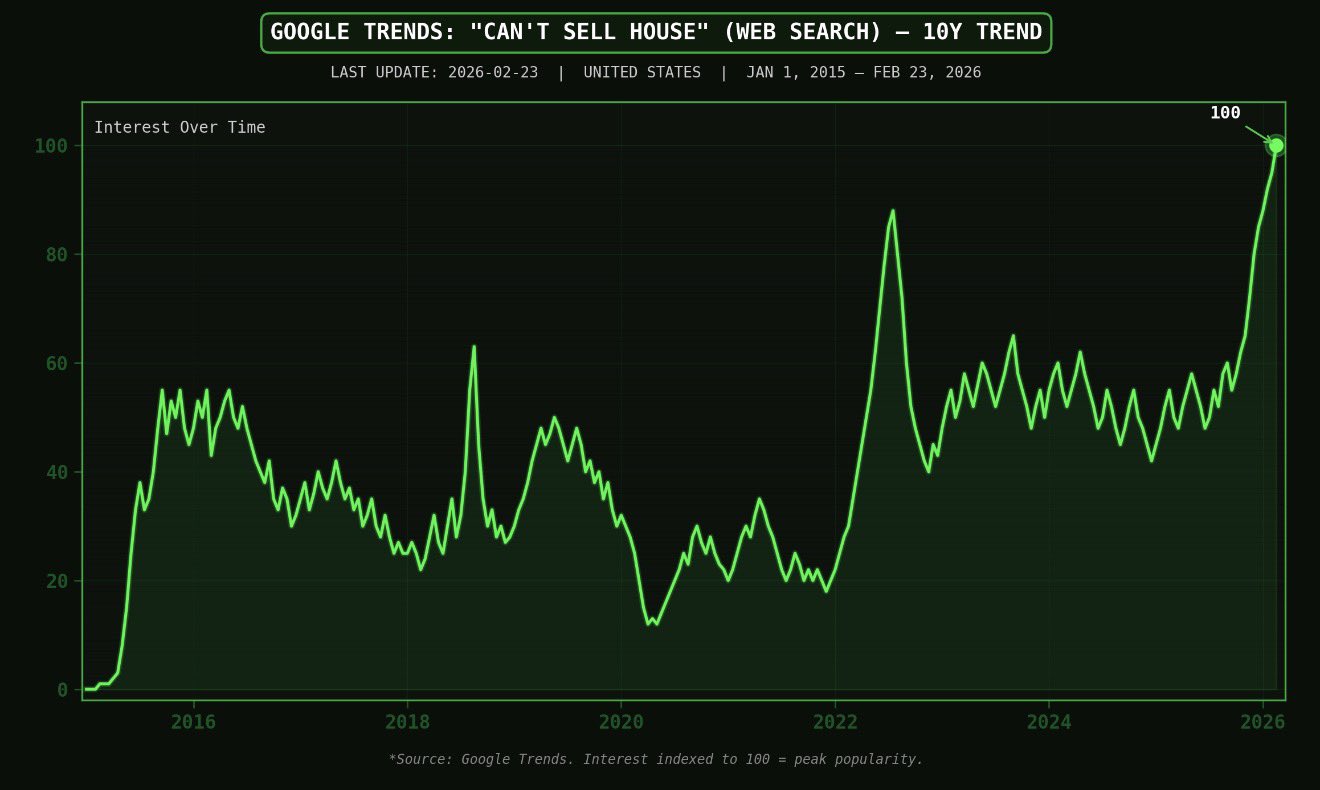

Housing Is Psychology Before It Is Math

Before prices fall, before listings spike, and before analysts revise their forecasts, something else changes first, and that is consumer confidence. Search behavior often reveals that shift before headlines do. Recently, searches for “can’t sell house” have climbed to record levels. That does not automatically signal a crash, but it does indicate that sentiment is changing. Sellers are beginning to question their pricing power. Buyers are becoming more selective. Conversations are shifting from urgency to caution.

Housing markets rarely collapse overnight. They transition. Inventory tends to build gradually. Days on market begin to stretch. Price reductions become more common and less surprising. Buyers regain leverage and take more time before committing. This is how cycles turn, not through panic, but through hesitation.

What’s Happening in Moncton Specifically?

The Moncton housing market experienced remarkable appreciation between 2020 and 2022. During that period, we saw strong migration from Ontario and other provinces, historically low mortgage rates, extremely tight inventory, increased investor participation, and intense competition among buyers. It was a powerful bull cycle fueled by extraordinary conditions.

But conditions have changed... Today, in Moncton, Dieppe, and Riverview, mortgage rates remain elevated compared to pandemic lows. Affordability has tightened. Buyers are more cautious and deliberate in their decision-making. Inventory levels, while not excessive, are higher than the extreme tightness we experienced at the peak. Price growth has slowed noticeably.

That does not automatically mean we are entering a downturn. It does, however, suggest that leverage is shifting. If you’re curious what homes are currently available and how pricing compares across neighbourhoods, you can browse current Moncton homes for sale to see real-time inventory conditions.

Are Moncton Home Prices Going Down?

The honest answer is that it depends on the segment.

Properties that are overpriced, require significant renovations, or sit in oversupplied pockets may experience downward pressure. On the other hand, turnkey homes in desirable neighbourhoods and properties with unique or limited supply characteristics may hold their value more effectively. Real estate is hyper-local. A detached home in Grove Hamlet will behave differently than a duplex near Université de Moncton. Market conditions vary not only by city, but by street and price range.

If you’re unsure where your home stands in today’s environment, you can request a free home value estimate in Moncton to understand your specific equity position.

How Broader Economic Data Applies to Moncton

Macro trends matter, even at the local level. Interest rate movements in the United States influence Canadian bond markets. Consumer psychology crosses borders. Investor capital flows globally. Migration patterns adjust based on affordability and opportunity. When confidence weakens in larger housing markets, it often influences buyer sentiment in Canada as well. Confidence drives transactions. Transactions influence pricing. Pricing affects household equity.

If you’re considering nearby communities as well, you can see current inventory in Dieppe and Riverview to compare pricing trends and supply dynamics across Greater Moncton.

Final Thoughts

Real estate markets move in cycles, and Moncton is no exception. We benefited from an extraordinary bull run during the pandemic years, fueled by record-low interest rates, migration trends, and tight supply. That environment no longer exists. Today we are operating in a different macroeconomic climate, one shaped by higher borrowing costs, slower demand growth, elevated consumer debt levels, and rapid technological change that is increasing productivity across industries.

If these broader trends continue, the most likely outcome is not a crash, but a normalization. That may look like slower appreciation, flat pricing across many segments, and mild downward pressure in oversupplied pockets. Buyers may regain negotiating power, and selling timelines may extend compared to the peak frenzy years. Normalization can feel uncomfortable after a strong bull market, especially for those who became accustomed to rapid gains. But market recalibration is a natural and often healthy part of long-term cycles.

If you would like a personalized breakdown of your neighbourhood, your property, or your long-term strategy, I am always available to walk through the numbers with you.

Whether you think prices are going up or coming down, the right move depends on your specific situation, timeline, and financial position. I help buyers and sellers make decisions based on data, not emotion. If you want to talk through what the current market means for your next move, let's connect.

Book a Call with Joel | Get Your Free Home Value

Joel Langlois | Moncton Real Estate

Local expertise • Data-driven pricing • Strategic marketing

Categories

Recent Posts