Moncton Buyer’s Guide

A step-by-step guide to buying a home in Moncton, Dieppe, and Riverview. Learn how to prepare financially, navigate inspections and offers, and buy with confidence in New Brunswick’s real estate market.

Delivered instantly to your inbox. No spam, ever.

What You’ll Learn Inside the Moncton Buyer’s Guide

+ Representation + negotiation sections (pages 7–8)

+ Buyer roadmap (page 9)

+ Inspection checklists (pages 10–12)

+ Local + relocation prep (pages 13–17)

and so much more....

GET YOUR COMPLETE HOME BUYING GUIDE -------->>

HOW BUYING A HOME IN GREATER MONCTON WORKS

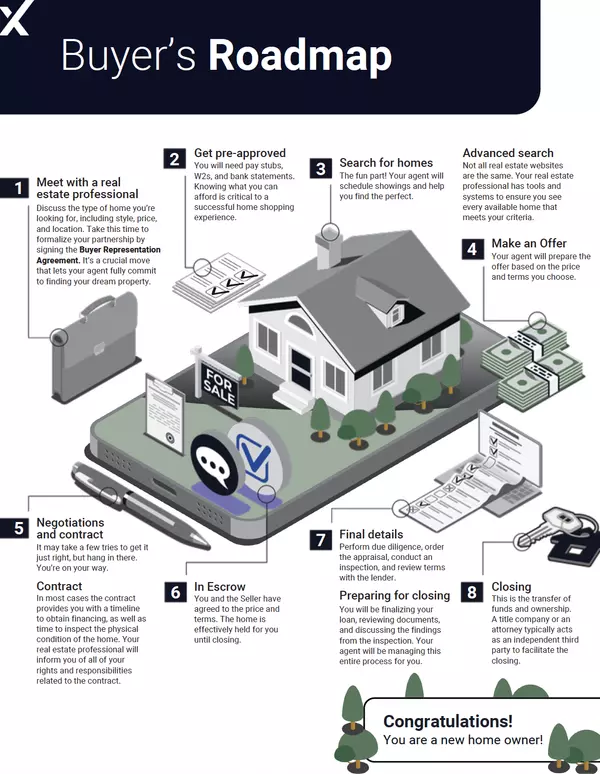

Step 1: Understand Your Budget and Get Pre-Approved

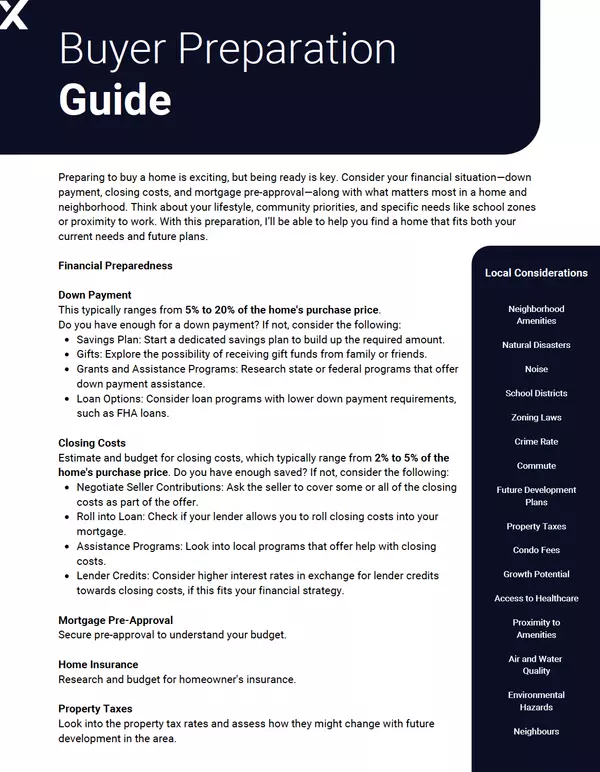

Before you start browsing listings, the first step is understanding what you can realistically afford. A mortgage pre-approval from a lender tells you your maximum purchase price, your estimated monthly payment, and the interest rate you qualify for. In New Brunswick, most lenders require a minimum credit score of 600-650 for conventional mortgages, though higher scores unlock better rates. Pre-approval is different from pre-qualification. Pre-qualification is an informal estimate based on self-reported income. Pre-approval involves a credit check, income verification, and document review. Sellers and listing agents take pre-approved buyers more seriously because it signals that financing is already in progress.Step 2: Define Your Search Criteria

Greater Moncton offers a range of communities, each with a different character. Moncton itself is the urban centre with the widest variety of housing stock, from older character homes in the North End to newer subdivisions in the northwest. Dieppe attracts families with its parks, trails, French-language schools, and newer construction. Riverview is quieter and more residential, with strong schools and river access. Beyond the tri-cities, areas like Shediac, Memramcook, and Salisbury offer larger lots and lower price points at the cost of a longer commute. I help buyers narrow their search by matching lifestyle priorities to specific neighbourhoods. Commute time, school zones, walkability, property taxes, and future development plans all factor into the decision.Step 3: Search, View, and Evaluate Properties

Once your budget and location preferences are established, we set up a customized listing search that sends new properties directly to your inbox as they hit the market. In a competitive market, seeing homes early matters. I also monitor coming-soon listings and off-market opportunities when they arise. During viewings, I walk you through what to look for beyond the surface: age of the roof, HVAC systems, foundation condition, water/sewer vs. well/septic, insulation quality, and potential renovation costs. Many homes in Greater Moncton were built in the 1970s-1990s and may have deferred maintenance that is not immediately obvious.HOW BUYING A HOME IN GREATER MONCTON WORKS

Step 4: Make an Offer and Negotiate

When you find the right property, we prepare a written offer that includes the purchase price, deposit amount, closing date, and any conditions. Common conditions in New Brunswick include financing approval, home inspection, and property disclosure review. For rural properties, well water testing and septic inspection conditions are standard. Negotiation in the Moncton market varies by price range and neighbourhood. Some properties receive multiple offers within days, while others sit long enough to allow room for negotiation. I provide a comparative market analysis for every property so you know exactly where your offer sits relative to recent sales.

Step 5: Inspections, Financing, and Due Diligence

Once your offer is accepted with conditions, the clock starts on your due diligence period. A home inspection typically costs $400-$600 in New Brunswick and covers structure, electrical, plumbing, HVAC, and exterior. I coordinate inspections with trusted local inspectors and attend on your behalf if needed, which is common for out-of-province buyers purchasing remotely. During this period, your lender finalizes the mortgage approval, your lawyer conducts a title search, and any additional inspections (septic, well, radon) are completed. I keep all parties aligned on timelines to ensure nothing falls through the cracks.

Step 6: Closing and Taking Possession

Closing in New Brunswick typically happens through a real estate lawyer. You will need to bring your down payment, pay closing costs (budget 1.5% to 3% of the purchase price), and sign the transfer documents. Closing costs include legal fees, land transfer tax, title insurance, and property tax adjustments.

On closing day, the title transfers, funds are exchanged, and you receive the keys. I make sure the transition is smooth and that you have contacts for local utilities, insurance, and any post-closing services you may need.

Why Work With Joel Langlois

I have helped over 250 families buy and sell across Greater Moncton. My approach is straightforward: clear communication, data-driven pricing guidance, and a process designed to eliminate surprises. Whether you are a first-time buyer, upgrading, investing, or relocating from another province, I tailor the experience to your specific situation.

Ready to start your search? Book a call and I will walk you through the process based on your timeline and goals.

FREQUENTLY ASKED QUESTIONS (FAQ'S)

How much do I need for a down payment in New Brunswick?

In Canada, the minimum down payment depends on the purchase price. Homes under $500,000 require as little as 5% down. For homes between $500,000 and $999,999, a blended minimum applies. A 20% down payment is required to avoid mortgage default insurance. I can help you understand what makes the most sense based on your situation.

What is the difference between a mortgage pre-qualification and pre-approval?

What are closing costs, and how much should I budget?

How does my credit score affect my mortgage rate?

What's included in my monthly mortgage payment?

How long does the home buying process usually take?

What's the first step to buying a home?

Can I buy a home while selling my current one?

What conditions are common in New Brunswick offers?

How competitive is the Moncton market right now?