First-Time Home Buyer in Moncton NB: Programs, Costs, and Market Conditions in 2026

Moncton's real estate market is shifting in a direction that benefits first-time buyers for the first time in years. Inventory levels have climbed to a five-year high, days on market are stretching, and the aggressive bidding wars of 2022 and 2023 have largely disappeared. For anyone who has been sitting on the sidelines waiting for conditions to improve, this is the window.

The average single-family detached home in the Greater Moncton area reached $420,900 as of Q4 2025, up 5.5% year over year, but the pace of appreciation has moderated. Combined with stable borrowing costs and several federal and provincial programs designed to reduce the upfront capital burden, first-time buyers in Moncton have more tools available to them right now than at any point in the past three years.

Programs and Incentives Available to First-Time Buyers in New Brunswick

The federal and provincial governments have stacked several programs that, when used together, significantly reduce the capital requirements for a first purchase. Here is what is available in 2026.

First Home Savings Account (FHSA): This account allows contributions of up to $8,000 per year, with a lifetime cap of $40,000. Contributions are tax-deductible (similar to an RRSP), and withdrawals for a qualifying home purchase are completely tax-free. If you started contributing when the program launched, you could have up to $24,000 in tax-sheltered savings available for your down payment right now.

Home Buyers' Plan (HBP): First-time buyers can withdraw up to $60,000 from their RRSP tax-free to purchase a home. Repayment is required over 15 years. This can be combined with the FHSA, meaning a single buyer could theoretically deploy up to $100,000 from registered accounts toward a purchase.

First-Time Home Buyers Tax Credit: A non-refundable federal tax credit worth up to $750 in the year of purchase. Modest, but it offsets a portion of closing costs.

NB Home Ownership Program: For households earning under $40,000, the province offers a repayable loan of up to $75,000, covering up to 40% of the purchase price. Interest-free for incomes under $30,000, with a graduated rate above that. This is particularly relevant for single buyers or those purchasing in more affordable areas like Moncton's north end or Salisbury.

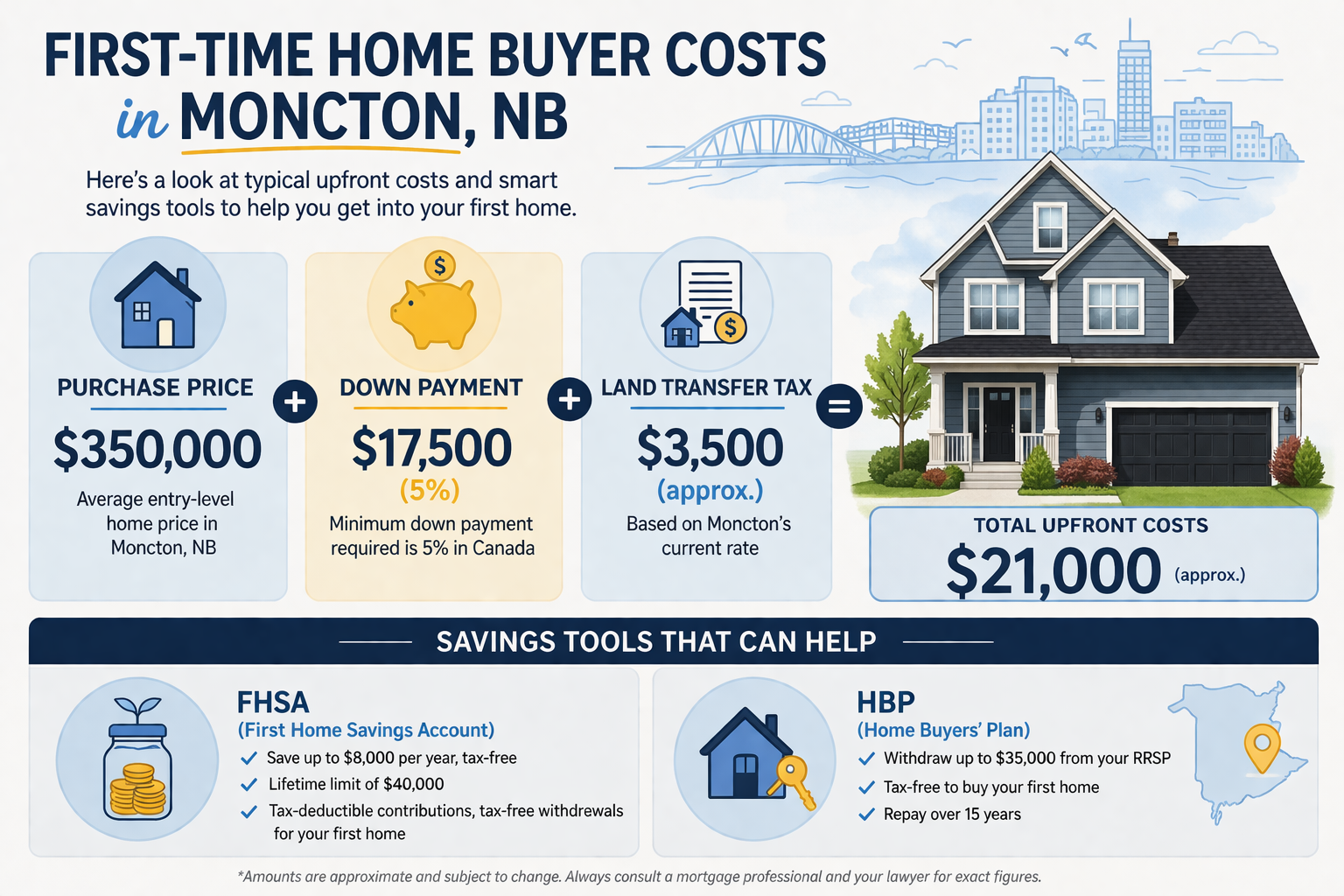

Land Transfer Tax: New Brunswick charges a flat 1% on the purchase price. On a $350,000 home, that is $3,500. There is no first-time buyer rebate on this tax, so budget for it in your closing costs.

Why Moncton's Market Favours First-Time Buyers Right Now

The shift toward balanced market conditions is the single most important factor for entry-level buyers. When inventory was tight in 2022 and 2023, first-time buyers were routinely outbid by repeat buyers with larger down payments, no financing conditions, and more flexibility on closing dates. That dynamic has eased considerably.

Inventory at a five-year high means more choice. Longer days on market means more time to conduct due diligence, negotiate conditions, and secure financing. Sellers are increasingly willing to accept offers with standard financing and inspection conditions, which is exactly the kind of offer a first-time buyer typically writes.

The price sweet spot for first-time buyers in Moncton sits between $250,000 and $400,000. At $350,000, the minimum down payment is $17,500 (5%), and CMHC mortgage insurance adds approximately 4% to the loan amount. Monthly carrying costs on a $332,500 mortgage at current rates will run approximately $1,900 to $2,100 depending on your amortization and rate, which compares favourably to average rents for comparable properties in the $1,400 to $1,700 range when you factor in equity accumulation.

What It Means for Buyers and Sellers

First-time buyers should approach this market strategically, not emotionally. Get your pre-approval locked in before you start viewing properties. Know your total budget including closing costs: land transfer tax, legal fees (typically $1,200 to $1,800), home inspection ($400 to $600), and any immediate repairs. Surprises at the closing table are the fastest way to start your ownership journey under financial stress.

If you are using the FHSA and HBP together, coordinate the timing of withdrawals with your mortgage broker and lawyer. The FHSA withdrawal must be for a qualifying home purchase, and the HBP withdrawal has specific rules around repayment schedules. Getting both right maximizes your tax efficiency and minimizes your out-of-pocket costs.

Sellers listing properties in the $250,000 to $400,000 range should be aware that their buyer pool is increasingly composed of first-time purchasers. This means offers will typically include financing and inspection conditions. Pricing competitively and presenting the property well will attract more qualified buyers and reduce time on market.

Local Insight

The biggest mistake I see first-time buyers make in Moncton is not treating the purchase as a financial decision. They focus on finishes, paint colours, and curb appeal while ignoring the neighbourhood trajectory, the property tax assessment trends, and the resale potential. Your first home is not your forever home for most people. It is a capital deployment decision that should set you up for your second move in five to seven years.

Right now, the best value for first-time buyers in Moncton sits in the north end, Lewisville, and parts of the west end where you can find detached or semi-detached homes under $350,000. These areas have solid rental demand if you need to convert the property to an investment later, and they benefit from the city's infrastructure spending and ongoing neighbourhood development across Moncton.

Moncton's north end offers some of the best value for first-time buyers with detached homes under $350,000 and strong rental conversion potential.

Ready to Make a Move?

If you are a first-time buyer in Moncton, the next step is getting clear on your numbers, your timeline, and your target neighbourhoods. A conversation with a local Realtor who understands the market at a street-by-street level will save you time and money.

Browse homes for sale in Moncton, NB

Check your current home value

Contact Joel Langlois

Read the complete Buyers Guide

Try the Mortgage Calculator

Joel Langlois | Moncton Real Estate

Local expertise • Data-driven pricing • Strategic marketing

Looking to invest in Moncton or Dieppe real estate? Get a targeted analysis of available multi-family and investment properties.

Book an investment consultation with Joel Langlois: sellingwithjoel@gmail.com

Disclaimer: Financial figures, tax rates, and program details referenced in this article are based on publicly available information as of April 2026. Program eligibility, rates, and terms may change. Consult a mortgage broker, financial advisor, or legal professional for advice specific to your situation. This article is for informational purposes only and does not constitute financial or legal advice.

Categories

Recent Posts